Oh, what a difference a few days can make, eh? We’ve gone from headlines screaming, “U.S. Heading for Recession!!” to ones talking about the greatest stock market rally in decades. And all it took was one announcement that the U.S. and China are getting closer to a trade deal that benefits both nations.

Of course, like clockwork, the naysayers came out in force questioning the validity of a joint statement made by the representatives of both countries. They say it’s just talk. It’s not a deal until it’s signed. The U.S. caved…

But really they just don’t want to admit that Trump was right…

He was right about trade imbalances. And he was right about tariffs. Maybe they’re not the most delicate tool. In fact, they’re more like a baseball bat than a surgeon’s scalpel. But nonetheless, Trump was right…

He knew that, as the world’s biggest consumer, the United States was a market nobody can afford to lose. And he knew that, while it might sting American consumers a little bit to pay more for their imported goods (or just buy American 🤷), it would hurt the other countries a lot more to lose their biggest buyer.

He knew that they’d come to the U.S. looking to make a deal. And that’s exactly what they did…

South Korea, Japan, Mexico, Canada, the United Kingdom, India, Israel, Switzerland, Qatar, Cambodia, France, Italy, and now China, too. They all decided it was better to make a deal than to try to carry out a trade war with America.

Trump even told people to go out and buy stocks. He said the “smart money” was being stupid and that you should always bet on American exceptionalism.

And markets are up over 20% since then.

The bottom line is the mainstream media was wrong and Trump was right, whether they’ll admit it or not. But I’m not here just to rub dirt in the mainstream media’s eyes while it’s down…

Because they’re probably not going to admit it. And that’s doing investors a huge (or should I say “yuge”) disservice. Because while they’re lamenting the fact that Trump was right about tariffs, investors need to start asking what Trump will be right about next…

The mainstream media isn’t going to tell you. That’s for sure. They can’t even admit he’s been right about pretty much everything else. Why would they start now?

But that’s what we’re here for, to set aside any personal feelings we might have and dig into the biggest investment opportunities. And, like Trump who’s busy building relationships all over the newly dubbed Arabian Gulf, we’re not resting for a second.

Because we knew exactly what Trump’s going to be right about next and it’s going to make a trade deal with China look like small potatoes.

That’s because Trump’s next big win has already been set in motion and he’s just cementing it and doing a victory lap through the oil-rich Gulf states…

You see, it’s a pretty commonly known fact that Donald Trump supports the U.S. fossil fuel industry. (Drill, baby, drill!). But it’s not as commonly understood that Trump doesn’t just want American energy independence. He wants American energy dominance.

And, quietly, earlier this year, he established a new national council dedicated to achieving just that:

This council is tasked with streamlining permitting processes, enhancing energy production and distribution across all sectors—including critical minerals—and fostering private sector investment by reducing regulatory barriers and promoting innovation.

And it’s already getting to work developing a comprehensive National Energy Dominance Strategy, coordinating federal and private sector efforts, and consulting with state, local, and tribal officials to expand reliable and affordable energy production nationwide.

Now, of course, the mainstream media is doing everything it can to hide the council’s success…

But savvy investors are already quietly reaping the rewards as certain American companies are thriving under these policies, but they remain completely off the radar of the general public.

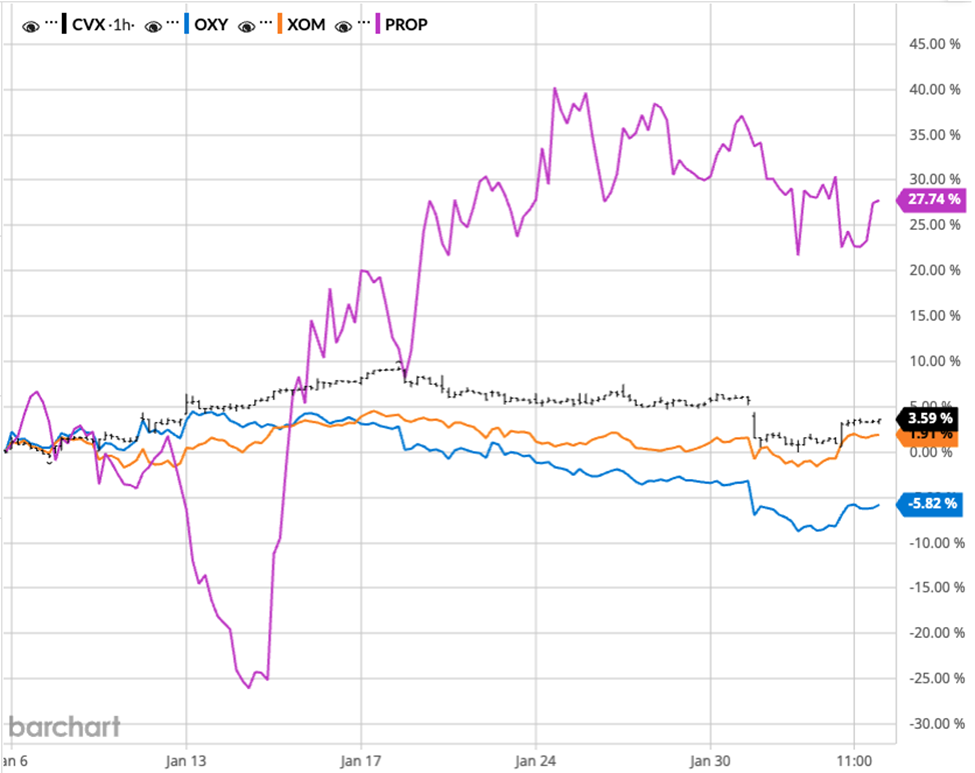

One in particular, Prairie Operating Company (NASDAQ: PROP) deserves particular attention. Since Trump instated his new energy policies, it’s grown production by over 1,000% through strategic acquisitions and expanded drilling.

Prairie is focused on the lucrative, but low-cost Denver Julesburg (DJ) Basin in northeastern Colorado. And it’s concentration of assets in oil-friendly, rural Weld County makes it a perfect investment for growth…

With no towns or communities close to its oil-rich assets, the company is able to move quickly to get its wells in the ground and the oil flowing out and down the pipelines to Cushing. And, as an added bonus, that oil gets a premium price at the pump down there because it’s better suited to the Gulf-coast refineries.

So, it’s got a low-cost field, a low-cost operation, direct access to the global hub for oil sales in Cushing, AND it gets a premium on its product because it’s what the refineries need. With breakeven prices potentially dropping below $40 in the near future, this company’s profitable when others aren’t.

Yet, it’s still relatively unknown outside of closely knit investment circles. But more and more investors are catching on. And the administration’s deregulation efforts and strategic appointments are now attracting global investment by the trillions (see Saudi Arabia’s $600 BILLION).

By streamlining regulations and opening new areas for exploration, the U.S. is solidifying its position as a global energy leader. This isn’t just about politics, though. It’s about profits…

Like I said, you shouldn’t expect to hear this story from the mainstream press – they’re too busy pushing their anti-Trump narratives.

That’s why they missed out on the record-setting rally the markets just had. But we’re willing to look past our own beliefs in search of profit opportunities for our investors.

And while the media unfortunately often lies to you, the numbers don’t. Prairie is one of the only places both the Trump administration and investors can look for growth in the American oil field.

Its strong balance sheet, low breakeven price, enviable location, and experienced leadership team make it the best bet for investors looking to capitalize on Trump’s next win while the mainstream media is still lamenting his last.